Introduction

Private equity has vital position in the investment industry– being able to generate significant profits for investors. This investment strategy revolves around the distribution waterfall, which illustrates how the returns earned by a private equity fund are split among the investment fund’s participants. The private equity waterfall also plays an important role in the field, as it outlines the conditions of profit sharing between the parties involved. This article explains the distribution of waterfalls, explaining what they are, their different parts, the different phases, the various forms, and most importantly, the matters that need to be considered by the investors.

Basics of Private Equity Fund Structures

A private equity fund is a collective fund of money raised and managed by private equity firms from institutional and accredited investors to invest in the equity of private companies. The private equity fund structure typically involves two primary stakeholders: Limited Partners (LPs) are the sources of capital and on the other hand, and General Partners (GPs) are responsible for the administration of the fund and the investment process.

Several stages are involved in the formation of a private equity fund, and these are—

-

The Fundraising Stage

-

The Investment Stage

-

The Management Stage

-

The Exit Stage.

In the fundraising phase GPs seek capital contributions from LPs. After an adequate amount is accumulated, the fund enters the investment phase in which GPs source, purchase, and oversee the portfolio firms—adjusted from the management phase, value creation activity is carried out to improve the portfolio companies’ performance. Lastly, the exit phase involves the realization of returns for the LPs and GPs through the sale of investments by listing the company on a stock exchange via mergers, acquisitions, or initial public offerings (IPOs).

What is a Distribution Waterfall?

A distribution waterfall is a strategic format used in private equity funds to split profits between the Limited Partners (LPs) and the General Partners (GPs). It ensures the order that payback is made concerning specified individuals and performance indices. The private equity waterfall can be broken in several steps, each with clear objectives in terms of distribution.

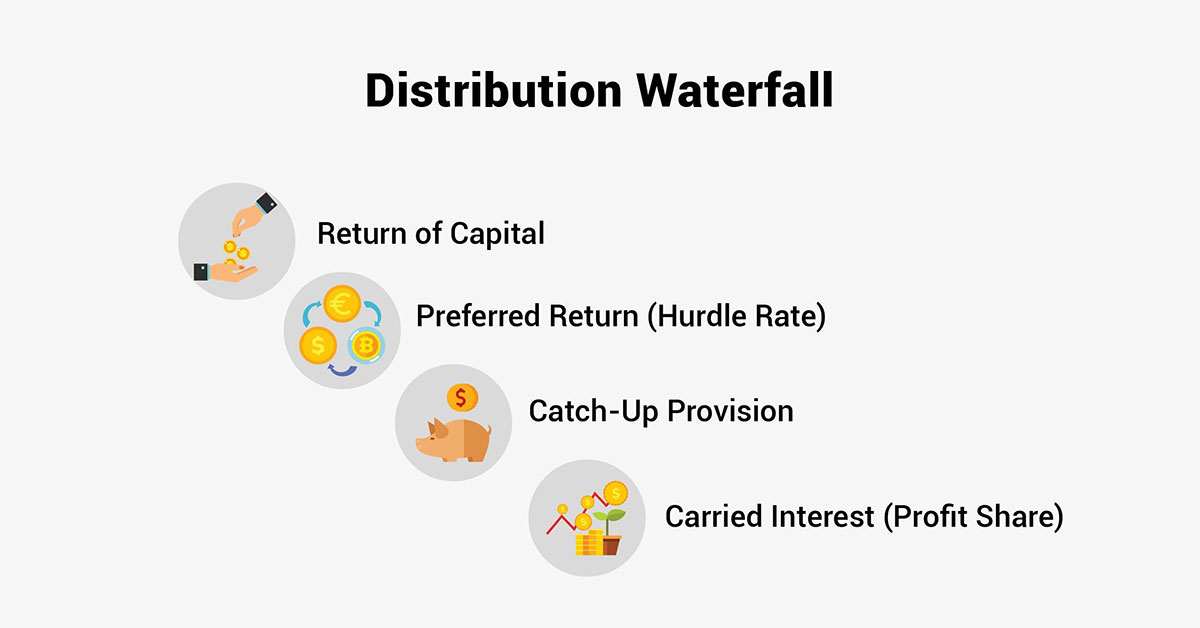

Key components of a distribution waterfall include:

-

Return of Capital: It is the sum of money provided initially by LPs that is paid back the moment the profits are earned.

-

Preferred Return (Hurdle Rate): LPs get a fixed percentage on the amount they invest with the company before the GPs can get their cut of the profits. This rate is generally 8 percent.

-

Catch-Up Provision: The majority of the time, GPs receive a preferred return and then a share of the profits until they make up for a required percentage of the total profits.

-

Carried Interest (Profit Share): The remaining profits are then distributed between the LPs and the GPs according to a certain ratio which may be 80/20 in favor of the several LPs.

The concept of the distribution waterfall controls the shares of the profits between the LPs and the GPs in a way that entices the GPs to perform while satisfying the LPs. Investors need to comprehend this particular mechanism to establish the expected returns and also to identify the respective self-serving motives of all the participants.

Example of a Distribution Waterfall

The distribution waterfall is directly related to the private equity fund because of which understanding each segment is essential to know how profits are divided among the parties interested.

-

Return of Capital:

The first level of the distribution waterfall is where all distributions are made to the LPs with a view of recovering their invested capital. For example, if LPs have invested USD 10 million, the initial USD 10 million of any return on the investment goes directly to the LPs before any share is given to the GPs.

-

Preferred Return:

After the invested capital has been retrieved, partners are mostly assured of an 8% preference income. This simply implies that the LPs must be given an 8% annual return on the capital they invested in the fund before the GPs can earn any proportional share of the profits earned. For example, should the LPs’ preferred return rate be 8%, they would get USD 800,000 in preference to any other distribution before proceeding to subsequent distributions in the formula.

-

Catch-Up Provision:

Following the LPs having taken their preferential share, the distribution is known as the catch-up, which means that GPs take a larger cut of the profits. For example, the subsequent USD 2 million of profits might be distributed to the GPs until they reach the amount that was agreed on for ‘catching up,’ so that the GPs obtain an appropriate percentage of total cash flows.

-

Carried Interest/Profit Share:

The last step is the division of the final profits according to the stipulated conditions; most commonly, 80% goes to LPs, and the rest, 20%, goes to GPs. For example, once the LPs have gotten their money back and their preferred return and the GPs get their pro rata, future profits might be split 80/20 in favor of the LPs and in favor of the GPs respectively to align the incentives of the two parties in the private equity fund.

Variations in Distribution Waterfalls

Distribution waterfalls can differ greatly depending on the agreed terms between the LPs and the GPs within the context of a private equity fund. These variations affect the way returns are split and may affect the incentives of both LPs and the GPs. Investors need to evaluate the proposed returns and liability for each of the structures when investing in private equity.

-

European Waterfall: Payments are made to LPs after all invested capital has been spent and the preferred return is given out. This structure is slightly conservative because LPs get their money back before any GPs get theirs.

-

American Waterfall: It is executed on a deal-by-deal basis, which enables GPs to capture their carried interest from successful deals before LPs have been able to recover their entire invested capital. This may result in GPs receiving their carry earlier while for the LPs this has the potential to be risky.

-

Modified American Waterfall: A blend to some extent of pure approaches to carried interest where GPs receive carried interest only when some conditions or indexes are fulfilled. This distribution is much fairer than the standard American waterfall in terms of the risk and reward of LPs and GPs.

-

Tiered Waterfall: This includes having different levels of returns with different carried interest percentages in each level. When returns rise, GPs may be entitled to a higher percentage of profits, thus encouraging improved performance.

Legal and Regulatory Aspects

Distribution waterfalls refer to the provisions in an investment fund that determine the order in which the profits are going to be split between the LPs and the GPs. Once an investment has been made it is important to ensure that both the LPs and the GPs understand distribution waterfalls to avoid scrupling legal and regulatory issues.

Key considerations include:

-

Legal Counsel: Hire professional lawyers to draw and negotiate waterfall provisions, so they are clear and easy to implement.

-

Compliance: It is also necessary to abide by rules and regulations recommended by organizations such as the SEC to minimize penalties on the private equity fund.

-

Documentation: It is recommended that all documents regarding the Distribution Waterfall are properly stamped systematically to ensure that all the parties who are involved in the distribution of the profits and other benefits from the project can refer to the documents when the need arises.

-

Industry Best Practices: Aim at meeting all the market efficiency standards regarding the equitable distribution of returns.

These legal tools help manage risks and ensure that the distribution process complies with the legal frameworks and investors’ demands for stability, giving credibility in the private equity market.

Conclusion

Investors and stakeholders in private equity industries need to be conversant with the various forms of distribution waterfall mechanisms. These structures regulate the distribution of profits in a way that is logical and reasonable, such that LPs and GPs are both satisfied. Understanding private equity waterfalls, their peculiarities, and their differences enables wise decision-making and high performance. A lot of attention should be paid to the analyz is and negotiations of the waterfall terms; it is always recommended to turn to a specialist in this area. When distribution waterfalls are implemented with the right knowledge, and through the right strategy, the investment experience and the results in private equity can be significantly improved.